Payment Gateway High Risk Your Essential Guide

Imagine a standard payment gateway is like a smooth, well-paved highway designed for everyday cars. A payment gateway high risk solution, on the other hand, is like a custom-built, all-terrain vehicle. It’s engineered from the ground up to navigate treacherous landscapes, specifically for businesses that financial institutions have flagged as ‘high-risk.’

This label often comes down to the industry you're in, your business model, or even a past history of chargebacks.

What Is a High Risk Payment Gateway

Simply put, a high-risk payment gateway is a specialized financial service that lets businesses in certain industries accept online credit and debit card payments. Where a standard processor might see too much liability, these gateways step in, backed by acquiring banks willing to take on the added risk.

It's crucial to understand that this classification isn't a judgment call on how you run your business. It's a risk assessment made by the payment processors themselves. For many legitimate companies, getting a standard merchant account is a non-starter; they're often turned away by acquirers wary of sectors known for high chargeback rates or heavy regulatory oversight. This is where specialized gateways become absolutely essential for survival and growth.

Why Are Some Businesses Considered High Risk

So, what gets a business slapped with the 'high-risk' label? It usually boils down to a few key factors, with the most common one being a high potential for chargebacks—those pesky transaction reversals a customer can initiate with their bank. Industries that rely heavily on recurring billing or sell digital goods often find themselves dealing with more customer disputes.

The 'high-risk' label isn't a penalty; it's a recognition that your business operates in a space that requires more robust security, underwriting, and fraud management. It signifies the need for a payment partner equipped to handle that complexity.

Other common red flags for processors include:

- Your Industry: Certain sectors are automatically considered high-risk. Think online gaming, travel agencies, subscription boxes, and adult entertainment.

- Big-Ticket Sales: If you're selling expensive items, the financial loss from a single fraudulent transaction is much greater, making your business seem riskier.

- Reputational Risk: Businesses operating in legal gray areas or those that attract public scrutiny often need a processor who understands their unique challenges.

- Selling Globally: Accepting international payments brings a whole new level of complexity, from currency conversions to cross-border fraud, which ramps up the risk profile.

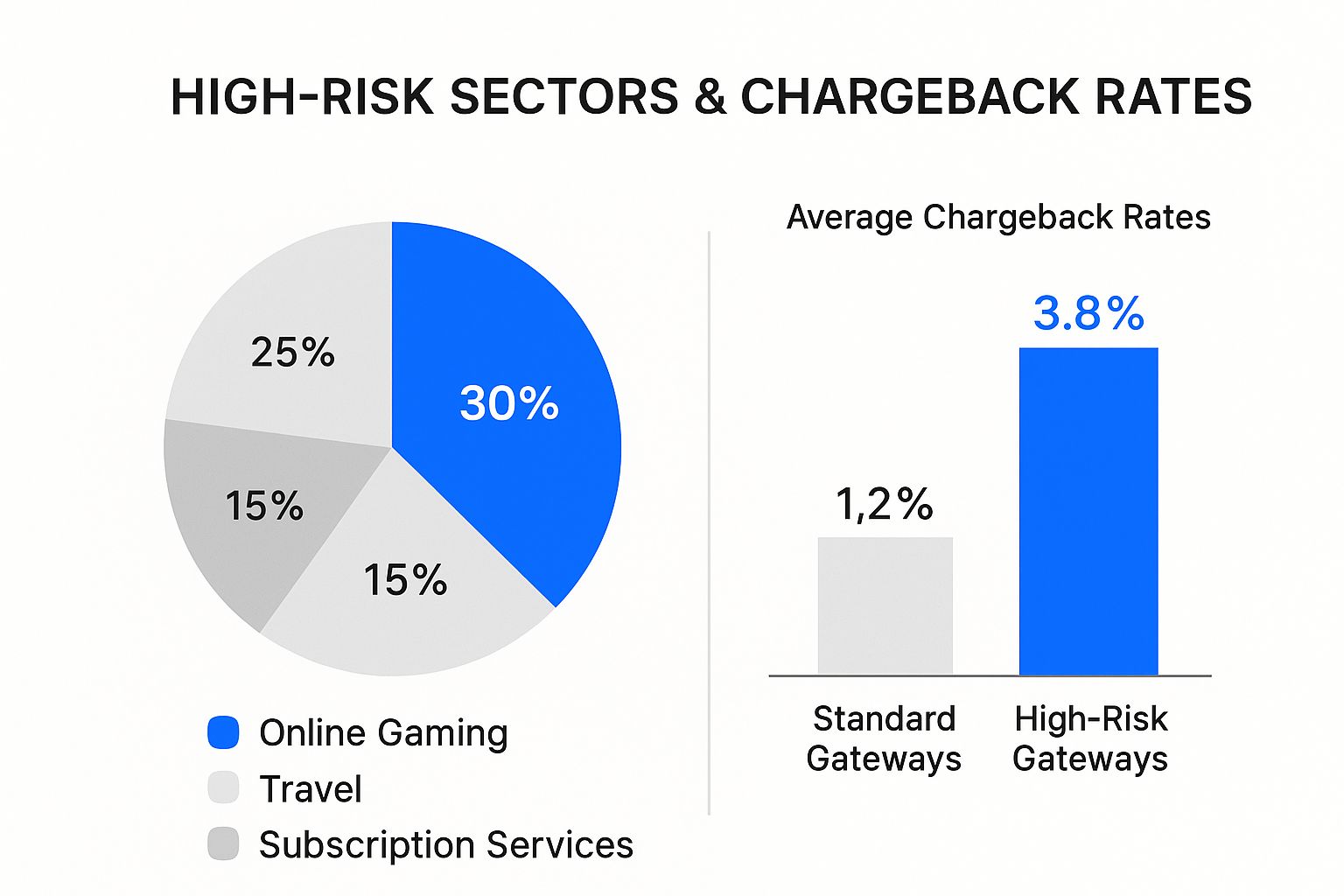

This infographic gives you a good look at how different high-risk sectors stack up and the kind of chargeback rates they're dealing with.

As the data shows, high-risk gateways are built to handle a much higher volume of chargebacks. That's precisely why they come equipped with more sophisticated tools and a stronger underlying infrastructure.

The Role of Specialized Processors

High-risk businesses—like those in travel, online gambling, or adult entertainment—often get shut out of standard merchant accounts because of high transaction volumes and the constant threat of fraud. This means they need a payment gateway built for their world, one that can manage higher chargeback rates and navigate complex transactions.

You'll find that a high-risk merchant account typically comes with higher fees than a standard one, which is just the processor's way of balancing out the increased risk. If you're interested in the bigger picture, you can learn more about the trends impacting financial institutions and their risk assessments over on JPMorgan's website.

Ultimately, a payment gateway high risk provider is more than a service; they're a critical business partner. They bring the essential fraud prevention tools, chargeback mitigation services, and—most importantly—the established relationships with acquiring banks that are actually willing to underwrite these accounts. Without them, a huge number of legitimate online businesses would be cut off from the digital economy, unable to process a single payment. They are the bridge connecting these merchants to the global marketplace.

Does Your Business Fall into a High-Risk Category?

It's not always obvious whether your business is considered "high-risk." While some industries get that label automatically, the tag often comes from how you operate, not just what you sell. It really boils down to understanding what makes payment processors nervous in the first place.

Think of it from their perspective. A processor's biggest headaches are chargebacks and fraud. Any business model that cranks up the probability of either is going to set off alarm bells. For example, a company selling expensive digital software is inherently riskier than a local coffee shop—digital goods are prime targets for fraud and tend to get more customer disputes.

This kind of risk math is exactly why a payment gateway high risk provider does more than just glance at your industry. They dig deep into your specific operations to get the full picture.

Understanding the "Why" Behind the Label

Being called high-risk isn't a judgment call on your business's quality. It’s a financial calculation based on a few key factors. It’s less about being in a "bad" industry and more about navigating a space with built-in financial volatility.

Processors are typically weighing a combination of things:

- High Chargeback Ratios: Some industries, like subscription boxes or digital downloads, just naturally see more customers disputing charges. This alone is a major red flag.

- Regulatory Scrutiny: If you're in a legally murky or heavily regulated field—think CBD, online gaming, or nutraceuticals—you'll need a processor with specialized legal and compliance teams.

- Recurring Billing Models: Subscription services are fantastic for predictable revenue, but they're also prone to "friendly fraud." That’s when a customer forgets about a recurring charge, disputes it, and creates a chargeback.

- Reputational Concerns: Some traditional financial institutions simply won't touch industries like adult entertainment or online dating because they see them as a reputational risk.

Getting a handle on these core issues is the first real step toward finding a payment partner who actually gets what you do and is built to support it.

Common High Risk Industries and Their Associated Risk Factors

To make this more concrete, let's look at some common industries that need a payment gateway high risk solution and pinpoint exactly why. This isn't just a random list; it’s a cheat sheet for understanding the specific challenges that different business models present to acquiring banks.

A business isn't high-risk just because of its products. It's classified as high-risk because its business model, industry regulations, or transaction patterns create a higher probability of financial loss for the payment processor.

The table below breaks down this connection, helping you see where your own business might fit in.

Common High Risk Industries and Their Associated Risk Factors

| Industry | Primary Risk Factor | Secondary Risk Factor |

|---|---|---|

| Online Gaming & Casinos | High potential for chargebacks and fraud from player disputes and bonus abuse. | Strict, varying international regulations and licensing requirements. |

| Subscription Services | Recurring billing model leads to a higher rate of "friendly fraud" chargebacks. | Customer lifecycle management and potential for high customer churn. |

| Travel & Tourism | Long gap between payment and service delivery increases cancellation risk. | High average transaction values and vulnerability to economic downturns. |

| CBD & Nutraceuticals | Complex and evolving legal regulations at state and federal levels. | Claims about product effectiveness can lead to customer disputes. |

| Adult Entertainment | High chargeback rates and perceived reputational risk for acquiring banks. | Age verification requirements and content regulations. |

| Digital Goods & Software | Intangible nature of products makes fraud difficult to trace and disputes common. | Global customer base introduces cross-border transaction complexities. |

Seeing your industry here helps you get ahead of the conversation. You can anticipate the questions a high-risk processor will ask and prepare documentation showing you have solid measures in place to manage these risks. This kind of preparation not only strengthens your application but also lays the groundwork for a much more successful partnership.

What to Look for in a High-Risk Payment Gateway

When you're running a high-risk business, choosing a payment gateway isn't just about finding someone who will take you on. It’s about arming yourself with the right financial toolkit for the long haul. A top-tier high-risk gateway is more than a transaction processor; it's a financial shield, built with specific features to protect your revenue and keep your business stable in a pretty volatile world.

Think of it this way: trying to operate in a high-risk industry without these specialized tools is like sailing into a storm without a rudder. Standard, low-risk gateways just aren't built for the kind of turbulence you face every day. So, let’s break down the absolute must-have features that separate the best high-risk gateways from the rest.

Advanced Fraud Detection and Prevention

Let's be blunt: for a high-risk merchant, fraud isn't a matter of if, but when. The single most critical feature of any specialized gateway is its fraud detection suite. We're talking about something that goes way beyond a simple address check. The best systems use a multi-layered defense, analyzing hundreds of data points for every single transaction, all in real-time.

These tools are your frontline defense, sniffing out and blocking shady activity before it ever becomes a chargeback headache.

Here's what that defense looks like in practice:

- IP Geolocation: This tool instantly flags where a customer is, catching transactions from known high-risk countries or when the location doesn't match the billing address. It's a simple but powerful check.

- Device Fingerprinting: A fraudster might use dozens of stolen credit cards, but they often use the same computer or phone. This technology identifies that unique device, connecting the dots and shutting them down.

- Velocity Checks: This feature watches for unusual patterns, like a sudden flood of transactions from one IP address or card number in a short time. It's a great way to stop automated bot attacks in their tracks.

AI-Powered Security Measures

Today, the most sophisticated high-risk gateways are bringing in the heavy artillery: Artificial Intelligence (AI) and machine learning. These aren't just buzzwords. AI systems sift through mountains of transaction data to spot subtle, fraudulent patterns that a human or a simple rule-based system would completely miss.

AI is making a huge impact across the financial world for a reason. For instance, 58% of companies report that AI has made regulatory compliance easier, while AI-powered systems can slash fraud detection costs by up to 30%. For a high-risk business, those kinds of savings aren't just nice—they're essential for survival. You can dig into more of these payment processing stats over on Airwallex.com.

A gateway using AI isn't just reacting to fraud; it's predicting it. The system is always learning and adapting to new scam tactics, so your defenses are never out of date.

Comprehensive Chargeback Management Tools

While stopping fraud is priority number one, some chargebacks will inevitably slip through. That's where management tools come in. A solid payment gateway high risk provider will give you a powerful suite of tools designed to help you fight back against illegitimate disputes. The goal is to keep your chargeback ratio safely below the thresholds set by Visa and Mastercard.

Effective chargeback management usually includes:

- Real-Time Alerts: This is a game-changer. You get a notification about a customer dispute before it becomes an official chargeback, giving you a chance to issue a refund and avoid the penalty.

- Dispute Resolution Support: Fighting a chargeback requires solid evidence. Good gateways provide tools and support to help you quickly gather and submit everything needed to win your case.

Multi-MID and Load Balancing

This is one of the most powerful strategies a high-risk processor can offer. Instead of relying on a single Merchant ID (MID) from one bank, they give you access to several. This is your ultimate safety net. If one bank gets spooked by a chargeback spike and shuts down your account, you're not out of business. Your processor simply reroutes your transactions through another MID.

Load balancing takes this concept to the next level. It intelligently spreads your sales volume across your different MIDs. This prevents any single account from hitting its monthly processing limit or drawing unwanted attention. It’s a crucial technique for ensuring your business stays online and processing, no matter what happens behind the scenes.

It's no secret that high-risk payment processing costs more. The sticker shock can be real, but those higher fees aren't random—they're a calculated and necessary part of operating in this space. When you're in a high-risk industry, you’re playing by a different set of rules, and that includes the cost structure.

Think of it like getting insurance for a high-performance sports car versus a standard family sedan. The sports car policy is pricier because the risk is higher and the potential for a costly claim is greater. In the same way, high-risk processing fees are elevated to cover the significant financial exposure your payment processor takes on every time a customer clicks "buy."

These aren't just arbitrary markups. The extra cost directly funds the advanced security, in-depth underwriting, and specialized support needed to keep your merchant account open and running smoothly.

Breaking Down High-Risk Processing Fees

When you work with a high-risk provider, you’ll notice a few key fees that you wouldn't see with a standard, low-risk account like Stripe or PayPal. Getting a handle on what these are and why they exist is key to managing your finances without surprises. It helps you see them less as a penalty and more as an investment in your business’s stability.

Here are the most common fees you'll run into:

- Higher Transaction Rates: This is the big one. A low-risk business might pay around 2.9% + $0.30 per transaction. A high-risk merchant, on the other hand, could be looking at rates from 3.5% to 5% or even higher, depending on the specifics of their industry. That extra percentage is the processor's main shield against potential chargeback losses.

- Monthly Account Fees: High-risk accounts need a lot more active monitoring. Monthly fees, which can range from $25 to over $100, cover the ongoing oversight and dedicated support required to manage your account.

- Chargeback Fees: Every merchant gets hit with chargeback fees, but they're steeper for high-risk accounts. You can expect to pay between $25 and $50 for every dispute filed, which gives you a strong incentive to use the fraud and chargeback prevention tools your provider offers.

What Are You Actually Paying For?

So, where does all that extra money go? It's not just lining the processor's pockets. Those fees are funneled back into building and maintaining a robust infrastructure designed to protect both your business and theirs. You're essentially paying for a premium security detail that low-risk gateways simply don't need.

The price of a high-risk payment gateway directly reflects the resources required to manage that risk. You’re buying stability, security, and the peace of mind that comes with a partner who won't cut you loose at the first sign of trouble.

This investment typically goes toward:

- Intensive Underwriting: Before you’re even approved, a team of underwriters invests serious time digging into your business model, sales history, and financial health. This deep-dive vetting is an expensive but crucial first line of defense.

- Advanced Fraud Scrubbing: Sophisticated fraud detection systems, often powered by AI, are not cheap to build or maintain. Your fees help pay for the technology that weeds out fraudulent orders before they can turn into costly chargebacks.

- Chargeback Mitigation Programs: Many processors provide chargeback alert services. These systems give you a heads-up and a short window to issue a refund before a customer complaint officially becomes a chargeback, which is a lifesaver for your merchant account health.

- Rolling Reserves: Don't be surprised if your processor holds back a percentage of your revenue in a non-interest-bearing account. This is called a rolling reserve, and it acts like a security deposit to cover any future chargebacks. It's the processor's safety net, ensuring funds are available to settle disputes down the road.

How to Apply for a High Risk Payment Gateway

Getting a merchant account with a high-risk payment gateway provider can feel like a huge hurdle, but it doesn't have to be. If you prepare properly and understand what they're looking for, you can seriously improve your chances of getting approved. It’s less about passing a test and more about making a strong case for your business's legitimacy and stability.

Think of it this way: you're showing underwriters that you understand the risks involved and have a solid plan to manage them. Success really boils down to being organized, upfront, and picking the right partner from the get-go.

Step 1: Vetting and Choosing the Right Provider

Before you even think about gathering documents, your first mission is to find a provider that actually specializes in your industry. Not all high-risk processors are the same. Some are experts in the travel industry, others know the ins and outs of subscription models, and some focus entirely on online gaming. A provider who gets the specific challenges of your business is far more likely to approve you and offer reasonable terms.

Look for a partner with a proven track record. Dig into their reviews, ask for case studies, and make sure they have solid relationships with multiple acquiring banks. This is a big deal—it's your safety net, ensuring you can keep processing payments even if one of their banking partners gets cold feet.

Also, don't forget about the tech side. If your store runs on a platform like Shopify or WooCommerce, double-check that the gateway has a smooth plugin or API. A clunky integration is a recipe for lost sales and technical nightmares, so this is a crucial step.

Step 2: Preparing Your Documentation

Once you’ve found a provider you trust, it's time to get your paperwork in order. Underwriters need a full picture of your business to feel comfortable with the risk. Being meticulous here is non-negotiable and can seriously speed up the approval process, which is almost always longer than for a standard account.

Your application is your chance to tell your business's story. A well-organized, complete package shows you're a professional who takes compliance and risk management seriously.

Here’s a list of what you'll almost certainly need to provide:

- Business License and Articles of Incorporation: This is the basic proof that your business is a legitimate, registered company.

- A Voided Business Check: This simply confirms your business bank account details so they know where to send your money.

- Photo ID of the Business Owner: Standard identity verification to know who is behind the company.

- Recent Business Bank Statements: Expect to provide 3-6 months of statements to demonstrate financial stability and healthy cash flow.

- Payment Processing History: If you have past processing statements—even from an account that was shut down—hand them over. This data reveals your sales volume, average ticket size, and, most importantly, your chargeback ratio. A ratio under 1% is the gold standard, but be honest no matter what the numbers say.

Step 3: Submitting a Strong and Transparent Application

When you’re applying for a high-risk payment gateway, honesty isn't just the best policy—it's the only policy. Underwriters are trained to sniff out inconsistencies, and trying to hide something about your business model is a surefire way to get rejected.

Be completely upfront about what you sell and how you market it. Clearly describe your products or services, your customer acquisition strategy, and how you handle fulfillment. If your chargeback rate has been high before, don't sweep it under the rug. Instead, explain the concrete steps you’ve taken to bring it down, like implementing better fraud prevention tools or beefing up your customer service.

Finally, make sure your website is professional and 100% compliant. Underwriters will go through your site with a fine-tooth comb, so be sure you have:

- A clear, easy-to-find privacy policy.

- Detailed terms and conditions for customers to review.

- Visible customer service contact info, including a phone number and email.

- Accurate product descriptions and crystal-clear pricing.

A polished, compliant website signals that you're a trustworthy merchant. By taking these steps, you build a compelling case for your business and position yourself as a partner they want to work with, making approval much more likely.

Why High-Risk Gateways Matter for the Digital Economy

To really get the full picture, you have to see where high-risk payment processing fits into the absolutely massive world of global payments. It might seem like a niche corner of the market, but these gateways provide the essential plumbing that allows entire industries to exist and grow online.

Frankly, they are the financial backbone for legitimate businesses that traditional banks simply won't touch.

Without a payment gateway high risk solution, countless innovators and entrepreneurs would be completely shut out of e-commerce. It's not just about enabling a transaction; it's about fostering competition and giving diverse business models a chance to survive.

Powering Innovation and Niche Markets

Think about any industry that pushes boundaries or caters to a very specific audience. Online gaming, subscription box services, even health supplements—these are all sectors that standard payment processors often reject outright with their one-size-fits-all rulebooks.

High-risk gateways do the exact opposite. They dig in and perform deep, individual assessments for each business.

This hands-on approach means a promising startup in a tricky industry actually gets a fair shot. By taking on the extra risk, these gateways essentially become incubators for new ideas and business models that would otherwise never see the light of day.

As the digital world keeps changing, new sectors are always popping up with their own unique risk profiles. For a great example of this, you can explore the challenges in the crypto space with Decentralized Finance (DeFi) security risks and mitigation.

A Critical Piece of the Global Payments Puzzle

The scale of the digital economy is just staggering. The global payment processing market is enormous, with digital payments expected to hit a transaction value of USD 157 trillion by 2025. If you want to dive deeper into those numbers, you can find great insights at clearlypayments.com.

High-risk payment gateways ensure that a huge slice of this economy isn't left behind. They build the secure rails needed to process billions of dollars in transactions that would otherwise have no safe place to go.

Ultimately, these specialized services make the entire online marketplace stronger and more vibrant. They ensure that being a legitimate business—not just a low-risk one—is what matters for participating in global e-commerce. In today's economy, that support is more critical than ever.

Frequently Asked Questions

When you're diving into the world of high-risk payment processing, you're bound to have questions. It's a complex space, and getting straight answers is key to making the right call for your business. Here are some of the most common questions we hear from merchants just like you.

What happens if I try to use a standard gateway for my high-risk business?

Think of it like trying to use a regular family car for an off-road race—it's just not built for the environment and is destined to fail. Sooner or later, the low-risk processor will review your account, flag the high-risk activity, and shut you down.

This isn't just an inconvenience; they'll likely freeze your funds and close your account with no notice. You'll be left unable to take payments and scrambling to find a new provider. That's why it's so important to partner with a proper payment gateway high risk specialist from the start.

How long does it take to get approved for a high-risk account?

Unlike standard gateways that can approve you almost instantly, the application for a high-risk merchant account is much more hands-on. Underwriters have to do a deep dive into your business. They’ll be looking at everything from your financial statements and past processing history to whether your website is fully compliant.

The whole process can take anywhere from a few days to a couple of weeks. The best way to keep things moving? Submit a complete and honest application with all of your documents in order right from the get-go.

Can a high-risk business ever become low-risk?

It's definitely possible, but it takes time and a proven track record. To even be considered, you'd need to show a consistently low chargeback ratio (staying well under 1%) over a long period, alongside stable processing volumes and solid financials.

For businesses in industries automatically flagged as high-risk (like gaming or CBD), making this switch is nearly impossible, no matter how well you run your operation. But if your "high-risk" label is due to past processing issues, showing a solid year or more of low-risk behavior can open up conversations about better rates and terms.

Ready to accept crypto payments without the hassle of traditional high-risk approvals? ATLOS Crypto Payment Gateway provides a secure, no-KYC solution that puts you in control. Get started today at https://atlos.io.